Introduction to kfoldcv

kfoldcv.RmdThe main function in the cvwrapr package is kfoldcv which performs K-fold cross-validation (CV). In this vignette, we go through a series of examples showing how it can be used.

Examples

Vanilla glmnet

Let’s set up some fake data:

set.seed(1)

nobs <- 100; nvars <- 10

x <- matrix(rnorm(nobs * nvars), nrow = nobs)

y <- rowSums(x[, 1:2]) + rnorm(nobs)If we used glmnet’s cv.glmnet function to perform CV, the call would look like this:

An equivalent call using kfoldcv would look like this.

Apart from x and y, kfoldcv needs train_fun and predict_fun which are the training and prediction functions respectively.

The returned objects from kfoldcv and cv.glmnet are slightly different:

names(glmnet_fit)

#> [1] "lambda" "cvm" "cvsd" "cvup" "cvlo"

#> [6] "nzero" "call" "name" "glmnet.fit" "lambda.min"

#> [11] "lambda.1se" "index"

names(cv_fit)

#> [1] "lambda" "cvm" "cvsd" "cvup" "cvlo"

#> [6] "lambda.min" "lambda.1se" "index" "name" "overallfit"Importantly though, the CV computations are the same:

library(testthat)

expect_equal(glmnet_fit$lambda, cv_fit$lambda)

expect_equal(glmnet_fit$cvm, cv_fit$cvm)

expect_equal(glmnet_fit$cvsd, cv_fit$cvsd)

glmnet with function arguments

kfoldcv works with more complicated function calls as well. For example, let’s say we want to fit a binomial model with observation weights:

biny <- ifelse(y > 0, 1, 0)

weights <- rep(1:2, length.out = nobs)

set.seed(1)

glmnet_fit <- cv.glmnet(x, biny, family = "binomial", weights = weights)Here is the equivalent call with kfoldcv. We now have 3 extra parameters:

-

train_params: A list of function arguments to be passed totrain_funfor model-fitting (excluding the data matrixxand the responsey). -

predict_params: A list of function arguments to be passed topredict_funfor prediction (excluding the fitted modelobject, new data matrixnewxand the lambda sequences). Notice here that we had to passtype = "response"to the prediction function: this is becauseglmnetreturns the linear predictor by default, whereaskfoldcvexpects the predictions to be on the scale of the response variable. -

train_row_params: A vector of names of function arguments that should be subsetted when performing CV.

set.seed(1)

cv_fit <- kfoldcv(x, biny, family = "binomial",

train_fun = glmnet, predict_fun = predict,

train_params = list(family = "binomial",

weights = weights),

predict_params = list(type = "response"),

train_row_params = c("weights"))Again, the CV computations are the same:

expect_equal(glmnet_fit$lambda, cv_fit$lambda)

expect_equal(glmnet_fit$cvm, cv_fit$cvm)

expect_equal(glmnet_fit$cvsd, cv_fit$cvsd)

glmnet with exclude

Let’s look at a glmnet example with exclude. First, let’s create some data such that the x matrix is sparse:

set.seed(101)

x[sample(seq(length(x)), 4 * nobs * nvars / 5)] <- 0

y <- rowSums(x[, 1:2]) + rnorm(nobs)

foldid <- sample(rep(seq(5), length = nobs))Sometimes, we might want to exclude variables which are too sparse. In the code below, we exclude variables that are more than 80% sparse. From glmnet version 4.1-2 and later (not on CRAN yet at time of writing), we can pass a function to the exclude argument.

filter <- function(x, ...) which(colMeans(x == 0) > 0.8)

glmnet_fit <- cv.glmnet(x, y, foldid = foldid, exclude = filter)Of course, we could pass the filter along to kfoldcv via train_params:

cv_fit <- kfoldcv(x, y, train_fun = glmnet, predict_fun = predict,

train_params = list(exclude = filter), foldid = foldid)

expect_equal(glmnet_fit$lambda, cv_fit$lambda)

expect_equal(glmnet_fit$cvm, cv_fit$cvm)

expect_equal(glmnet_fit$cvsd, cv_fit$cvsd)If we have an earlier version of glmnet which only allows the exclude argument to take a vector of indices, we can use kfoldcv to achieve the same result:

train_fun <- function(x, y) {

exclude <- which(colMeans(x == 0) > 0.8)

if (length(exclude) == 0) {

model <- glmnet(x, y)

} else {

model <- glmnet(x[, -exclude, drop = FALSE], y)

}

return(list(lambda = model$lambda,

exclude = exclude,

model = model))

}

predict_fun <- function(object, newx, s) {

if (length(object$exclude) == 0) {

predict(object$model, newx = newx, s = s)

} else {

predict(object$model, newx = newx[, -object$exclude, drop = FALSE], s = s)

}

}

cv_fit <- kfoldcv(x, y, train_fun = train_fun, predict_fun = predict_fun,

foldid = foldid)

expect_equal(glmnet_fit$lambda, cv_fit$lambda)

expect_equal(glmnet_fit$cvm, cv_fit$cvm)

expect_equal(glmnet_fit$cvsd, cv_fit$cvsd)Some notes of caution are in order:

-

train_funmust take in the design matrix asxand the response asy. In its return value, it must have thelambdasequence as the named elementlambda. -

predict_funmust take in the output oftrain_funasobjectand the new data matrix asnewx. It must also have an argument (sby default) that takes in alambdasequence, andpredict_funmust return a matrix of predictions, each column corresponding to one value oflambda.

Other loss functions

The loss function used in CV is controlled by two function arguments: type.measure and family. To see all possible type.measure values for each family, run availableTypeMeasures():

availableTypeMeasures()

#> $gaussian

#> [1] "deviance" "mse" "mae"

#>

#> $binomial

#> [1] "deviance" "class" "auc" "mse" "mae"

#>

#> $poisson

#> [1] "deviance" "mse" "mae"

#>

#> $cox

#> [1] "deviance" "C"

#>

#> $multinomial

#> [1] "deviance" "class" "mse" "mae"

#>

#> $mgaussian

#> [1] "deviance" "mse" "mae"

#>

#> $GLM

#> [1] "deviance" "mse" "mae"The default is type.measure = "deviance" and family = "gaussian", which corresponds to mean-squared error. Below is an example of misclassification loss with a binary response:

biny <- ifelse(y > 0, 1, 0)

glmnet_fit <- cv.glmnet(x, biny, family = "binomial",

type.measure = "class", foldid = foldid)

cv_fit <- kfoldcv(x, biny, family = "binomial", type.measure = "class",

train_fun = glmnet, predict_fun = predict,

train_params = list(family = "binomial"),

predict_params = list(type = "response"),

foldid = foldid)

expect_equal(glmnet_fit$lambda, cv_fit$lambda)

expect_equal(glmnet_fit$cvm, cv_fit$cvm)

expect_equal(glmnet_fit$cvsd, cv_fit$cvsd)There seems to be a bit of duplication in that we have to specify family = "binomial" as an argument to kfoldcv() as well as in the list provided to train_params. This duplication is to allow for greater generality for train_fun. In glmnet, the type of model being fit is defined by an argument named family, so in theory we could extract the family value from train_params to determine the type of model being fit. However, not all model-fitting functions will have a “family” argument.

Principal-components (PC) regression

Let’s look at a non-glmnet example. Here, I want to do principal components (PC) regression and I want to cross-validate the number of PCs to include in the model. Let’s use our non-sparse fake data again:

set.seed(1)

nobs <- 100; nvars <- 10

x <- matrix(rnorm(nobs * nvars), nrow = nobs)

y <- rowSums(x[, 1:2]) + rnorm(nobs)The pls package can perform PC regression with pcr(), but its interface is quite different from what kfoldcv() needs. Recall that train_fun must take the data matrix, response and hyperparameter values as x, y and lambda respectively. predict_fun must take the output of train_fun, the new data matrix and the hyperparameter values as object, newx and s respectively. The code below shows how we can write train_fun and predict_fun for the PC regression problem:

library(pls)

# lambda represents no. of PCs

train_fun <- function(x, y, lambda) {

df <- data.frame(x, y)

model <- pls::pcr(y ~ ., data = df, ncomp = max(lambda))

return(list(lambda = lambda, model = model))

}

predict_fun <- function(object, newx, s) {

preds <- predict(object$model, newdata = newx, ncomp = s)

return(array(preds,

dim = c(nrow(newx), length(s))))

}

set.seed(2)

lambda <- 1:10

cv_fit <- kfoldcv(x, y, lambda = lambda,

train_fun = train_fun, predict_fun = predict_fun)kfoldcv() returns an object of class “cv_obj”, which is equipped with a plot method much like those for cv.glmnet objects. The code below shows how we might plot a CV curve for PC regression:

plot(cv_fit, log.lambda = FALSE)

Notice that in determining the lambda.1se value, the plot method correctly determined that it should be looking at smaller values of lambda (corresponding to fewer PCs), instead of larger values of lambda, as is usually the case in glmnet. How did it figure it out? When computing the lambda.1se value, kfoldcv looks for the smallest model such that its CV error is within 1 SE of the minimum CV error. In doing so, it assumes that the lambda sequence provided to it is ordered from smallest model to largest model. In this example, we provided lambda <- 1:10. Compare that to the glmnet examples, where lambda is ordered from largest to smallest.

Gradient boosting with gbm

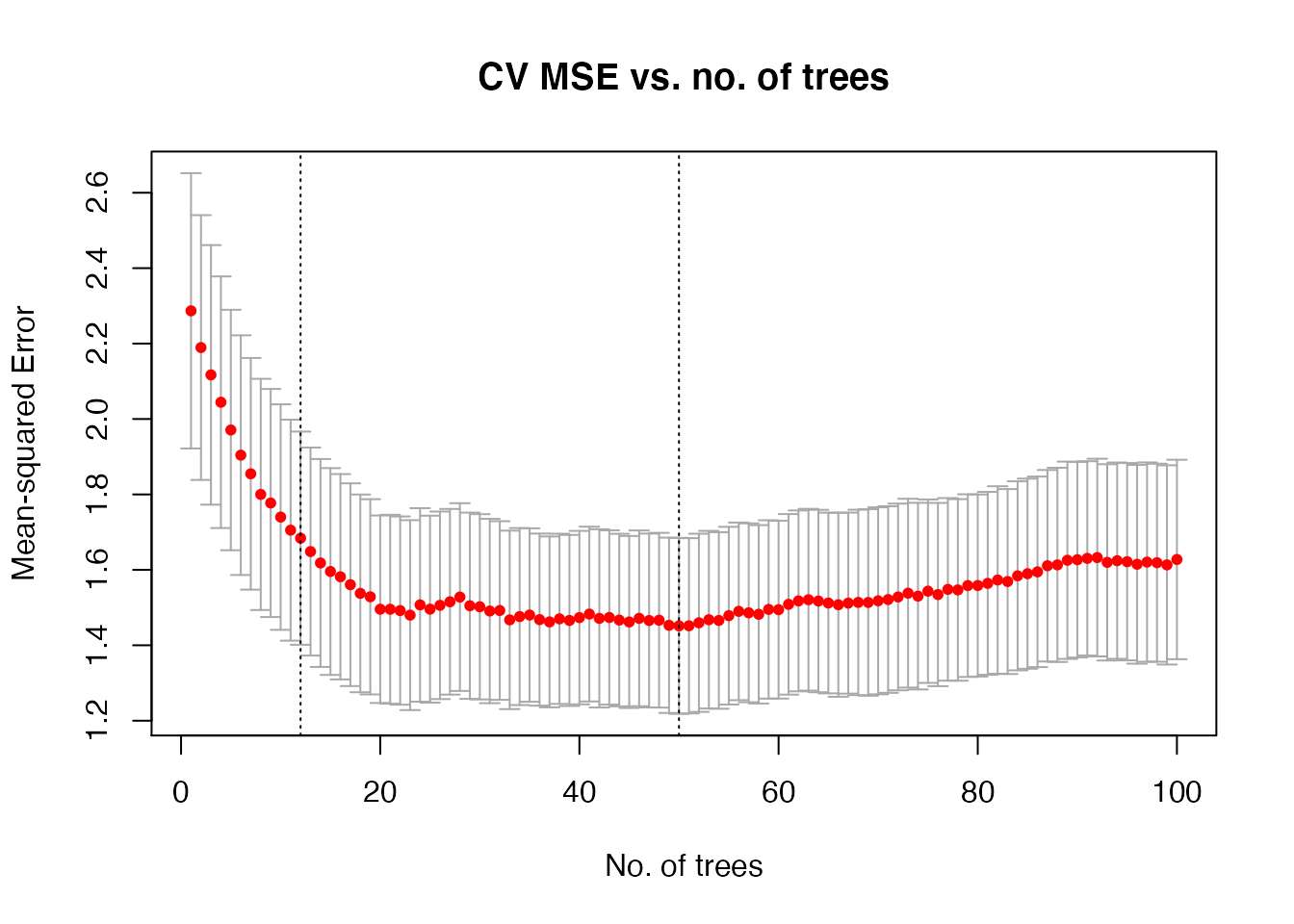

Let’s look at another non-glmnet example: gradient boosting with the gbm package. In this first example, we want to cross-validate the number of trees to be included in our boosting ensemble. As with PC regression, we need to write our own train_fun and predict_fun to interface correctly with kfoldcv.

library(gbm)

# lambda represents # of trees

train_fun <- function(x, y, lambda) {

df <- data.frame(x, y)

model <- gbm::gbm(y ~ ., data = df, n.trees = max(lambda),

distribution = "gaussian")

return(list(lambda = lambda, model = model))

}

predict_fun <- function(object, newx, s) {

newdf <- data.frame(newx)

predict(object$model, newdata = newdf, n.trees = s)

}

set.seed(3)

lambda <- 1:100

cv_fit <- kfoldcv(x, y, lambda = lambda,

train_fun = train_fun, predict_fun = predict_fun)Again, we can plot a CV curve. Notice how we can rename the x-axis and add a title:

plot(cv_fit, log.lambda = FALSE, xlab = "No. of trees",

main = "CV MSE vs. no. of trees")

Next, let’s try to cross-validate for a different parameter: interaction.depth. Notice that the internals of train_fun and predict_fun look quite different from before. This is because gbm has the ability to predict for any number of trees as long as it is smaller than that in the fitted model: this allows us to fit just one model for the whole lambda sequence. For interaction.depth, we will have to fit one model for each interaction.depth.

# lambda represents interaction depth

train_fun <- function(x, y, lambda) {

df <- data.frame(x, y)

model <- lapply(lambda, function(i) gbm::gbm(y ~ ., data = df,

interaction.depth = i,

distribution = "gaussian"))

return(list(lambda = lambda, model = model))

}

predict_fun <- function(object, newx, s) {

newdf <- data.frame(newx)

preds <- lapply(object$model,

function(obj) predict(obj, newdata = newdf,

n.trees = obj$n.trees))

return(matrix(unlist(preds), nrow = nrow(newdf)))

}

set.seed(3)

lambda <- 1:5

cv_fit <- kfoldcv(x, y, lambda = lambda,

train_fun = train_fun, predict_fun = predict_fun)

plot(cv_fit, log.lambda = FALSE, xlab = "Interaction depth",

main = "CV MSE vs. interaction depth")

Other functionality for kfoldcv

kfoldcv has a few other capabilities worth mentioning here:

-

foldid: An optional vector of values between1andnfolds(inclusive) identifying which fold each observation is in. Note thatkfoldcvactually works even iffoldiddoes not take values between1andnfolds, but for ease of use it is recommended that users do so. -

keep: If set toTRUE,kfoldcvreturns the matrix of pre-validated fits as well as thefoldidvector used in CV. Default isFALSE. -

save_cvfits: If set toTRUE,kfoldcvreturns the intermediate model fits for each CV fold. This is useful if the user wants to inspect the intermediate fits (e.g model coefficients) or compute some intermediate statistic (e.g. how many times a feature appears across the folds). However, bear in mind that this could greatly inflate the size of the objectkfoldcvreturns. Default isFALSE. -

parallel: If set toTRUE, model-fitting for each CV fold can be done in parallel. A parallel backend must be registered first. Below is a code example comparing a call tokfoldcvwith and without parallel computing, using the vanillaglmnetexample.

# without parallel computing

set.seed(3)

foldid <- sample(rep(1:5, length.out = nrow(x)))

cv_fit1 <- kfoldcv(x, y, foldid = foldid, train_fun = glmnet,

predict_fun = predict)

# with parallel computing

library(parallel)

library(doParallel)

cl <- parallel::makeCluster(2)

doParallel::registerDoParallel(cl)

cv_fit2 <- kfoldcv(x, y, foldid = foldid, train_fun = glmnet,

predict_fun = predict, parallel = TRUE)

parallel::stopCluster(cl)

# check that the two fits are the same

expect_equal(cv_fit1$lambda, cv_fit2$lambda)

expect_equal(cv_fit1$cvm, cv_fit2$cvm)

expect_equal(cv_fit1$cvsd, cv_fit2$cvsd)